Text | Retail Business Finance

On December 20, Xiaocaiyuan International Holdings Co., Ltd. (hereinafter referred to as “Xiaocaiyuan”) was listed on the main board of the Hong Kong Stock Exchange. As of the close, it closed at HK$9.66 per share, an increase of about 14%, and the total market value reached HK$11.365 billion.

Source: Snowball

Regarding the use of funds from this IPO (initial public offering), Xiaocaiyuan previously stated that the proceeds are expected to be used to continue to expand its store network, enhance supply chain capabilities, smart equipment and digital systems to improve information technology capabilities, etc.

Source: Xiaocaiyuan prospectus

Industry insiders believe that listing can provide a large amount of financial support for Xiaocaiyuan, which will help the company accelerate its expansion and enhance its brand influence. These funds can be used to open new stores, improve service quality, strengthen supply chain management, and conduct technology research and development to further consolidate and enhance the company’s market position.

The successful listing of Xiaocaiyuan means that the company’s brand value and popularity will be significantly improved, which will help attract more consumers’ attention and trust, and will also help to boost the confidence of catering companies in going public. You must know that since 2021, Catering companies such as Green Tea, Laoxiang Chicken, Village Base, and Yang Guofu have submitted prospectuses, but they have failed to knock on the door of the Hong Kong Stock Exchange.

Of course, we also need to objectively look at the growth potential of Xiaocaiyuan after its listing. After all, since this year, the average daily sales and same-store turnover rate of Xiaocaiyuan’s single stores in first-tier cities have declined. As for whether it can achieve “thousand stores” by the end of 2026 “The target depends on whether company management, supply chain, service quality, quality control, etc. can keep up with the rapid development of the brand in the short term.

It is worth noting that Xiaocaiyuan has a gambling agreement with Canadia Capital, which undoubtedly increases its financial risks. If the market value fails to meet expectations, it may have a significant impact on the company’s financial condition, including but not limited to equity dilution, tight capital flow and increased financial costs.

01 Scale changes performance, and style of play hides hidden dangers

The performance growth for three consecutive years actually hides the “single store anxiety” of Xiaocaiyuan.

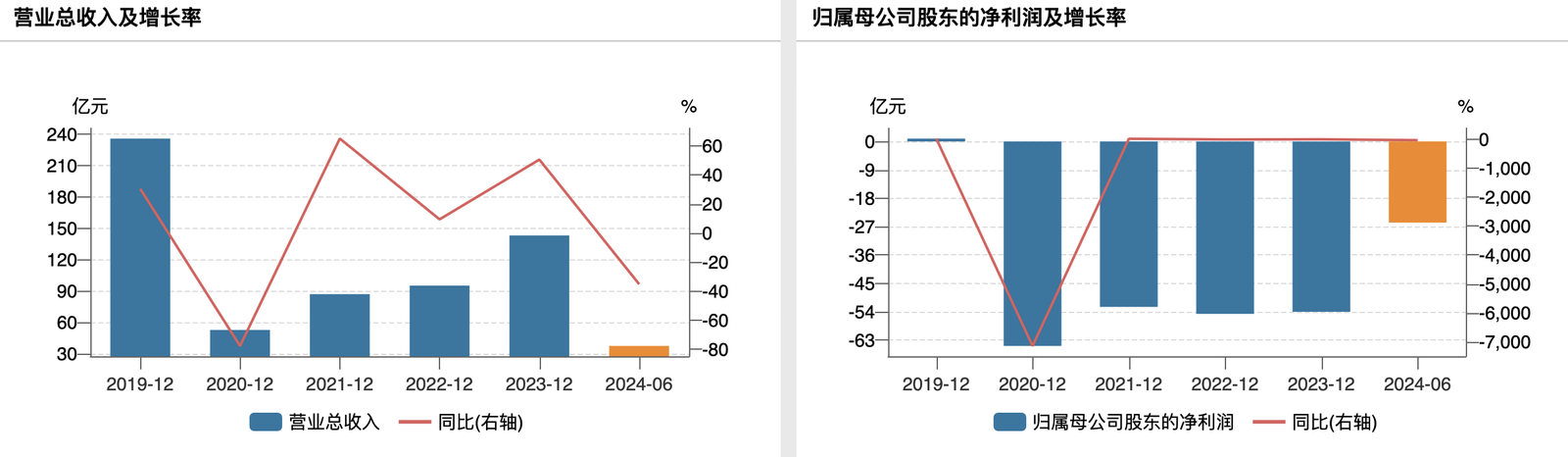

The prospectus shows that in 2021, 2022, 2023 and the eight months ending August 31, 2024, Xiaocaiyuan will achieve revenue of approximately 2.646 billion yuan, 3.213 billion yuan, 4.549 billion yuan and 3.544 billion yuan respectively.

Source: Xiaocaiyuan prospectus

The profits during the period were approximately 227 million yuan, 238 million yuan, 532 million yuan and 401 million yuan respectively. The net profit margins during the same period were 8.6%, 7.4%, 11.7% and 11.3% respectively. For the eight months ended August 31, 2024, compared with the same period in 2023, Xiaocaiyuan’s store-level operating profit margin dropped from 21.3% to 17.8%.

Despite the overall growth trend, Xiaocaiyuan’s single-store revenue has not kept up with the pace, and there has even been a “backlash.”

Since 2021, Xiaocaiyuan’s average daily sales per store have fluctuated between 23,000 and 29,000, of which the average daily sales for dine-in restaurants have been between 15,000 and 20,000. Compared with the same period last year, Xiaocaiyuan’s single-store dine-in daily sales and average daily customer volume in the first eight months of this year have both declined.

Not only that, the per capita consumption of dine-in food in Xiaocaiyuan is also declining. In the first eight months of 2023, it was 65.2 yuan. In the same period this year, it has dropped to 59.5 yuan, falling below 60 yuan.

Source: Xiaocaiyuan prospectus

Single store performance declined, but overall performance showed an upward trend. This may be related to Xiaocaiyuan’s relatively aggressive new store expansion strategy.

From 2021 to 2023, Xiaocaiyuan will open 107, 48, and 132 new stores respectively. From January to August 2024, Xiaocaiyuan continued to expand, opening 109 new stores and increasing the number of stores to 640. As of the Latest Practicable Date (i.e., November 28, 2024), Xiaocaiyuan has 663 directly operated stores (including 658 “Xiaocaiyuan” stores), covering 146 cities or counties in 14 provinces in China, mainly located in East China.

Source: Xiaocaiyuan prospectus

It can be seen that Xiao Caiyuan “evened” the declining performance of single stores through store expansion, and staged an expansion game of scale for performance. Or having tasted the benefits of expansion, Xiaocaiyuan chose to continue to increase the number of stores.

The prospectus shows that in 2021, 2022, 2023 and the eight months ending on August 31, 2024, Xiaocaiyuan will open 107, 48, 132 and 109 new stores respectively. The company plans to open approximately 160 and 180 new “Xiaocaiyuan” stores in 2025 and 2026 respectively.

Source: Xiaocaiyuan prospectus

Although the relatively aggressive store expansion strategy has helped Xiaocaiyuan achieve overall performance growth in the short term, it has many disadvantages in the long run.

Xiaocaiyuan is obviously aware of this, and stated in its latest prospectus: “We may not be able to open new stores at the same pace or as planned in the past. Delays or failures in opening new stores may have a negative impact on our growth strategy. and have a material adverse effect on our expected financial and operating results.”

On the one hand, Xiaocaiyuan is a direct operation model, and its chairman Wang Shugao once said “we will never engage in franchising.” However, the high asset investment under rapid expansion will naturally have an impact on cash flow.

Source: Xiaocaiyuan prospectus

In terms of the amount of investment in a single store and the payback period, according to the prospectus, the investment in opening a “small vegetable garden” store is expected to be between 1.3 million and 1.7 million yuan.

Among the stores that have achieved investment recovery as of August 31, 2024, the average investment recovery periods for stores opened in 2021, 2022 and 2023 are 17.3 months, 12.3 months and 9.4 months respectively. For Xiaocaiyuan stores opened during the track record period and which have achieved investment recovery as of August 31, 2024, the average investment recovery period is approximately 13.8 months. In contrast, in the popular Chinese catering market with a unit price of 50-100 yuan, the average investment payback period usually exceeds 18 months.

On the other hand, as the number of stores becomes more dense, it is bound to further dilute the revenue of a single store, which will lead to a vicious cycle of “single store decline – store opening – further decline”.

The current store distribution of Xiaocaiyuan shows strong geographical concentration, mainly concentrated in Jiangsu and Anhui provinces, with a small number of provinces involved.

Figure: Number of stores and revenue distribution of Xiao Cai Yuan in China

The above two points, the decline of single stores and concentrated geographical distribution, and the high investment in the direct operation model, are laying the foundation for more uncertain risks for Xiaocaiyuan’s subsequent more aggressive store expansion strategy.

In fact, since 2023, the hidden dangers of small vegetable gardens have been exposed.

According to the prospectus, in 2023 and the eight months ending August 31, 2024, Xiaocaiyuan will have 66 and 56 loss-making stores respectively, with total operating losses of 13.3 million yuan and 11.2 million yuan respectively.

This means that Xiaocaiyuan will open 132 new stores in 2023, but half of the stores have not achieved profitability. What is more noteworthy is that this is the data after excluding the stores that have been closed in that year. If added, it will reach There are nearly 100 stores, accounting for one-sixth of the current total number of Xiaocaiyuan stores.

It is true that the increase in store scale has painted a beautiful “report card” for Xiaocaiyuan, but the performance of a single store hidden under the “growth report card” is the core that determines how far Xiaocaiyuan can go.

Catering companies have always adhered to the “single store model” theory. Quantity is the “leaves” and the single store model is the branches. How can the branches be “luxuriant” when the branches are “full of holes”?

02 After emerging from “Anhui cuisine”, where will we go in the future?

“Anhui cuisine dinner” is the “ID card” of the small vegetable garden, and this positioning is gradually blurring.

Compared with its two powerful competitors, Green Tea Restaurant and Xibei Noodle Village, the biggest difference between Xiaocaiyuan is not only the niche status of “Anhui cuisine”, but also its blurring brand positioning, that is, the “fast food” of dinner. “.

This is reflected in many aspects. For example, Xiaocaiyuan is trying a variety of “fast food”-like business formats in order to “sink” better and faster. For example, the “Cai Shou” brand will be launched at the end of 2023, positioned as a community canteen, with locations concentrated near residential buildings, SKUs also streamlined to 36 types, and the unit price per customer has dropped to about 30 yuan.

Of course, these two changes are not simply “streamlining” or “sinking” attempts, but are intuitively reflected in the optimization of the financial performance of the small vegetable garden.

The most obvious one is Xiaocaiyuan’s advantage in cost control. The net profit margin will be 11.7% in 2023, which is higher than many competing brands in the industry. Compared with green tea, the highest is only 8.23%.

In addition, the declining pricing and positioning can also reduce the opening cost of a single new store, making Xiaocaiyuan’s vigorous store expansion plan more feasible.

But there are always two sides to the coin. In order to optimize the financial structure as much as possible to achieve the purpose of listing, the small vegetable garden has gradually begun to deviate from the original clear positioning.

Although the founder Wang Shugao’s background as an Anhui chef and the various promotions on Xiaocaiyuan’s own official website are always reminding him of the positioning of “New Anhui Cuisine”. However, when looking at the actual menu, there are very few dishes that meet the definition of true Anhui cuisine. Except for the well-known dish of stinky mandarin fish, the best-sellers on many lists are actually Hunan and Shandong cuisine such as “Chili Stir-fried Pork” and “Beijing Sauce Shredded Pork”. famous dishes.

As one of the eight major cuisines, Anhui cuisine does not have a strong reputation, and its heavy oil and salt characteristics also limit its widespread spread. Small vegetable gardens labeled as “New Anhui Cuisine” not only fail to strengthen memory points, but also make their positioning more ambiguous when adding new non-Anhui cuisine dishes.

On the other hand, for Green Tea and Xibei, the labels of “Jiangsu and Zhejiang Cuisine” and “Northwestern Cuisine” have always been very clear, and their impressions on mass consumers have become deeper.

Due to unclear positioning, the financial indicators of Xiaocaiyuan stores also showed a partial downward trend.

Taking the “table turnover rate”, the core indicator of catering companies, as an example, whether it is first-tier or second-tier cities and other other cities, as of the end of August 2024, the latest table turnover rate of Xiaocaiyuan has dropped to about 3 times. In third-tier and below cities, where Xiaocaiyuan contributes half of its revenue, the turnover rate is at the bottom among all city levels.

Source: Xiaocaiyuan prospectus

To make matters worse, Xiaocaiyuan’s per capita consumption of dine-in food has also begun to decline year by year. From 2021 to the first eight months of 2024, the per capita consumption was 66.1 yuan, 65.8 yuan, 65.2 yuan, and 59.5 yuan respectively, and the dine-in business is in Xiaocaiyuan accounts for the largest proportion of total revenue, at about 70%, and the remaining 30% is takeaway business and other businesses.

Source: Xiaocaiyuan prospectus

The performance of key indicators such as the slowdown in revenue growth, continued losses in stores, and decline in turnover rate and consumption volume all reflect the decline in the appeal of small vegetable gardens to consumers.

In this regard, in the prospectus, Xiaocaiyuan also explained one by one, saying that some data fluctuations from 2023 onwards were mainly due to the base effect caused by the rapid surge in consumer spending in the Chinese food market at that time, and the company also made adjustments to dish prices. cater to consumer preferences.

In the fiercely competitive domestic Chinese food market, for the sake of performance, Xiaocaiyuan has not strengthened its differentiated competitiveness to break through in the “Anhui cuisine” segment.

So, how to put aside the restrictions on cuisines and let more consumers accept it while achieving store growth while retaining its unique positioning as a “new Anhui cuisine” is a dilemma for Xiaocaiyuan.

Overall, the small vegetable garden currently has three major weaknesses and two major risks.

First, the industry threshold is low and competition is fierce, which places high demands on the company’s ability to sustain and operate efficiently.

Second, consumers have a strong willingness to try new products, but user stickiness is not high. They have higher requirements for the iteration of the company’s dishes and store environment.

Third, store performance is highly dependent on location selection, and there is a certain probability of making the wrong choice.

It is worth noting that Xiaocaiyuan has a gambling agreement with Canadia Capital.Based on the calculation that after the IPO, Canadia Capital holds 6.4% of the shares and the issuance market value is HK$10 billion, the value of Canadia Capital’s shareholding is HK$640 million (approximately 600 million yuan), a “net profit” of 100 million compared with the total investment of 500 million yuan.

The prospectus disclosed that if Xiaocaiyuan cannot be listed or the market value after listing is less than 130% of the valuation after the investment of the previous investors, it will issue new shares to Canada Capital for free or at the lowest price permitted by law, or it will issue shares to Canada Capital. Cash compensation.

Xiaocaiyuan’s involvement in the gambling agreement undoubtedly increased its financial risks. If the market value fails to meet expectations, it may have a significant impact on the company’s financial condition, including but not limited to equity dilution, tight capital flow and increased financial costs.

There is no doubt that food safety risks will also bring a huge crisis of trust to brands.

From 2021 to 2023, Xiaocaiyuan’s stores received 7 administrative penalties, which involved issues such as food safety, substandard tableware, and illegal operations. On the Black Cat Complaint Platform, many consumers also reported food safety issues such as foreign objects eaten in the vegetable garden and food poisoning. In July this year, a health certificate crisis broke out in Xiaocaiyuan.

For a listed company, food safety is the basic requirement as well as the bottom line and red line. The catering market is changing rapidly, consumer tastes are unpredictable, and market competition will not relax just because of its status as a listed company. Xiaocaiyuan has a long way to go.

For more exciting content, follow Titanium Media’s WeChat ID (ID: taimeiti), or download Titanium Media App