Text | Hong Kong Stock Research Society

Regarding involution, it is actually a label that CATL has always wanted to erase. Chairman Zeng Yuqun even stated at the Summer Davos Forum on June 25 that he did not know what the word “volume” meant.

“The last thing CATL does is compete on price, but rather focuses on competing on value.”

With the convening of the World Power Battery Conference on September 1, CATL Chief Technology Officer Gao Huan revealed the company’s strategic plan for battery swapping and began to explore “new” value.

According to Gao Huan, in the long run, CATL will build 10,000 battery swap stations across the country, which means that CATL will become an infrastructure-level enterprise in the global new energy field. In comparison, NIO, which has focused on battery swapping since its inception, currently has only about 2,500 battery swap stations deployed across the country.

As an upstream supplier of almost all new energy vehicle companies, why did CATL choose to increase its investment in the battery swap market at this time? What impact will CATL’s entry have on NIO, which has been deeply involved in this industry for many years? How long can the current situation of “one superpower and many strong players” in China’s new energy field continue?

Is it the right choice for “King Ning” to enter the battery swap industry?

In fact, as early as July 2020, CATL signed a vehicle-battery separation project contract with BAIC New Energy, officially entering the field of battery swap operations as a battery manufacturer. Since then, CATL has cooperated with Foton Zhilan, NIO and Nezha in battery swapping.

However, at that time, the battery swap model was still a niche model. According to data from the China Electric Vehicle Charging and Swapping Infrastructure Promotion Alliance, at the end of 2021, the total number of battery swap facilities in the country was only 1,298, of which the battery swap stations under NIO and another battery swap service operator, Aulton New Energy, accounted for the vast majority.It can be seen from this that at that time, CATL’s initial attempts at battery swapping were still in the “testing the waters” stage and did not cause significant changes in the industry..

However, with the increasing penetration rate of new energy in recent years, CATL’s attention and investment in the battery swap market have also been increasing.

On the one hand, CATL has increased its technological investment in the field of battery swapping.In 2022, it will launch the battery swap brand “Lexing Battery Swap” and “Chocolate Battery Swap Block” technology for the passenger car market, and will operate in many cities including Xiamen, Fuzhou, Hefei, and Guiyang.

On the other hand, since the beginning of this year, CATL has continued to make efforts in terms of partners in the battery swap market.In January 2024, CATL and Didi Chuxing established a battery swap joint venture, taking the lead in launching battery swap applications in online car-hailing scenarios. Subsequently, GAC Aion and BAIC Group also cooperated with CATL in the field of battery swap.

From waiting and watching to increasing sales, why did CATL choose to increase its investment in battery swapping now?According to Chen Weifeng, general manager of CATL’s subsidiary responsible for coordinating the battery swap business, CATL has several main considerations for entering the battery swap market:

First, with the growth of the new energy market and the increasing maturity of technologies such as extended-range and pure electric vehicles, users’ range anxiety has been greatly reduced. Therefore, after their range anxiety is met, users are more concerned about charging time and convenience.

From the user’s perspective, the battery swap mode is much faster than fast charging. Currently, the battery swap time of Aulton New Energy’s ultra-fast swap station is 20 seconds, and the battery swap time of NIO’s fourth-generation swap station is about 2 minutes. In comparison, it takes more than 30 minutes for fast charging products to charge from 10% to 80%.

Second, the maturity of related technologies has made it possible to popularize battery swapping. Previously, most battery swapping scenarios occurred in the fields of taxis and heavy trucks. Compared with commercial vehicles and taxis with relatively uniform specifications, the variety of sizes and body styles in the passenger car field make it difficult to unify battery specifications and sizes, which restricts the popularization of the battery swap model.

The launch of the chocolate battery swap technology by CATL covers most models of passenger cars from A00 to B and C, as well as logistics vehicles. The battery swap station can adapt to various models that use chocolate battery swap blocks, enabling freedom of choice of battery swap models.

From this perspective, CATL has already made some plans for the battery swap market. After years of waiting, it is the right choice for CATL to announce its entry into the market now that the market and technology are mature.

CATL and NIO are backstabbing each other

However, with the entry of companies of CATL’s size, it means that existing companies in the battery swap industry will face unprecedented impact.

In China, NIO is a loyal supporter of the battery swap model, the main force in the battery swap war, and one of CATL’s most feared opponents.At the beginning of August, NIO officially announced that the battery swap model had exceeded 50 million times, providing users with a total of 2.62 billion kWh of electricity. As of August 6, NIO has deployed 2,465 battery swap stations and 3,930 charging stations across the country, including 826 high-speed battery swap stations.

In the words of Li Bin, the founder of NIO, battery swapping is the “cloud computing” of new energy vehicles, and NIO will stick to the battery swapping business. In Li Bin’s view, NIO should think of battery swapping as AWS did with cloud services in 2003, not afraid of losses or time-consuming.

It is worth mentioning that in August 2020, CATL and NIO explored cooperation in the battery swap business. CATL and NIO jointly established a joint venture subsidiary to focus on the battery leasing business of “car-battery separation”. In January 2023, the two parties also signed a five-year comprehensive strategic cooperation agreement.

But beneath the harmonious surface, the secret struggle between this pair of good partners has been going on for a long time.

Li Bin once said in 2016 that he would not develop his own power battery, “We will use whoever’s battery is good.” But in 2022, the NIO Shanghai Battery Factory, which is equipped with 31 laboratories, was accidentally exposed, which also declared that Li Bin broke his promise. In the same year, CATL formed an alliance with Didi, ostensibly targeting the commercial market of online car-hailing. But it turns out that CATL eventually extended its tentacles to the equally vast passenger car market – just like NIO, which broke its promise and started to develop its own batteries.

On the surface, the attractive share of the battery swap market is an important reason for CATL to enter this field.

A report by iResearch Consulting pointed out that by 2025, the number of battery swap stations in China will reach 34,000, and the corresponding electricity consumption market and operation market sizes of battery swap stations are expected to be 35.5 billion and 61.6 billion yuan respectively. The average annual compound growth rates from 2021 to 2025 will reach 118% and 90% respectively.

(Image from iResearch)

But this is only the superficial reason.From CATL’s business perspective, battery swapping is not just a new project to make money, but also involves the company’s core business and competitive barriers.

For CATL, the battery swapping business is inseparable from the keyword “binding”. It is also related to the competition for the right to speak in the new energy vehicle industry and the layout of the entire industrial chain.

CATL wants to tie up with car companies. Previously, LG Energy and Panasonic increased their investment in China, and Guoxuan High-tech and BYD also caught up and eroded part of CATL’s territory. In fact, CATL does not have a good response to this. For example, the price issue, the hard cost of batteries is here. Even if CATL is willing to make concessions, it is still an “unbearable burden” for car companies suffering in the price war.

Therefore, CATL can only find another way, using batteries as an anchor to seek expansion opportunities in the upstream and downstream of the industrial chain and expand its influence on new energy vehicle companies. The only way that is most closely connected to power batteries and can most touch the pain points of car companies and users is battery replacement.

From this perspective, whether it is NIO or other car companies, although CATL has played an important role in their rise, interests are the eternal contradiction. The two sides have gone from symbiosis and win-win to mutual resentment and then to “backstabbing” each other, which is nothing more than a fight for the “cake”.

How long can the “one superpower and many strong countries” situation in the new energy field last?

In fact, it is not only NIO that has “broken up” with CATL. In the entire new energy vehicle field, “the world has suffered from King Ning for a long time”, and in recent years, the attitudes of major automakers towards “King Ning” have become increasingly entangled.

On the one hand, car companies have gradually begun to avoid the more expensive CATL in their lowest-equipped models and choose products from lower-priced battery companies such as Xinwangda, and second- and third-tier power battery companies have begun to rise.

Previously, Ideal changed its previous practice of only using batteries from CATL and added two new partners, Honeycomb Energy and Sunwoda. Xiaopeng Motors also switched to using products from battery manufacturers such as Sinotruk, Honeycomb Energy, and EVE Energy because of the large price increase of batteries from CATL.

On the other hand, car companies have also begun to choose to bypass third-party power battery suppliers and choose to build their own battery factories.BYD, Tesla, Geely, GAC, Xiaopeng and other car companies are all building their own power battery projects.

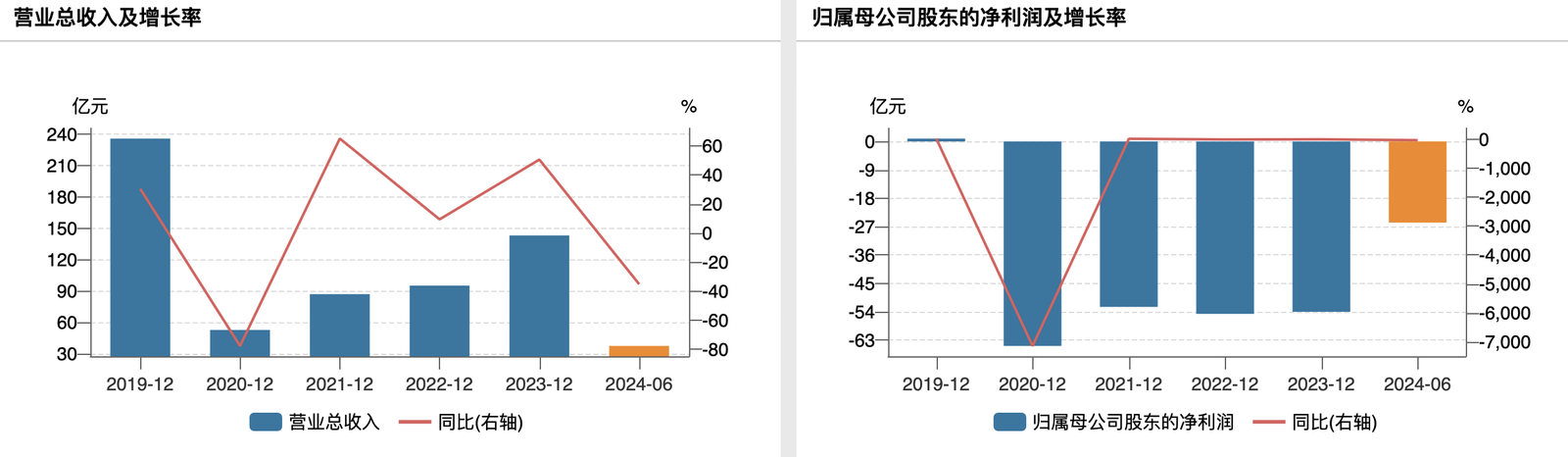

Under the joint “resistance” of car companies, CATL achieved operating income of 166.767 billion yuan in the first half of 2024, a year-on-year decrease of 11.88%, showing a decline in revenue for the third consecutive quarter. At the same time, CATL’s capacity utilization rate fell to 65.33%. From this perspective, compared with the skyrocketing revenue and record stock prices in 2020 and 2021, the glorious era of “King Ning” may have ended.

However, CATL is also actively looking for the second and third growth curves, hoping to continue its position in the industry. Judging from recent business trends, in addition to the battery swap mentioned above, CATL has launched the “New Energy Life Plaza” event in the ToC business line, and launched the after-sales brand “Ningjia Service” for C-end consumers, and began to build a consumer brand. At the same time, CATL has also explored the field of vehicle batteries for water and air transportation. In November 2022, it established a subsidiary specializing in electric ships; in July 2023, it cooperated with COMAC to establish a joint venture to develop electric aircraft.

From this perspective, in the iteration of the industrial wave, even a strong company like CATL, the former king, may stand on the edge of the cliff at any time today, or be ruthlessly washed away by the waves tomorrow. In this competition with no end in sight, whether CATL can have the last laugh remains to be seen.

For more exciting content, follow Titanium Media WeChat ID: taimeiti, or download the Titanium Media App