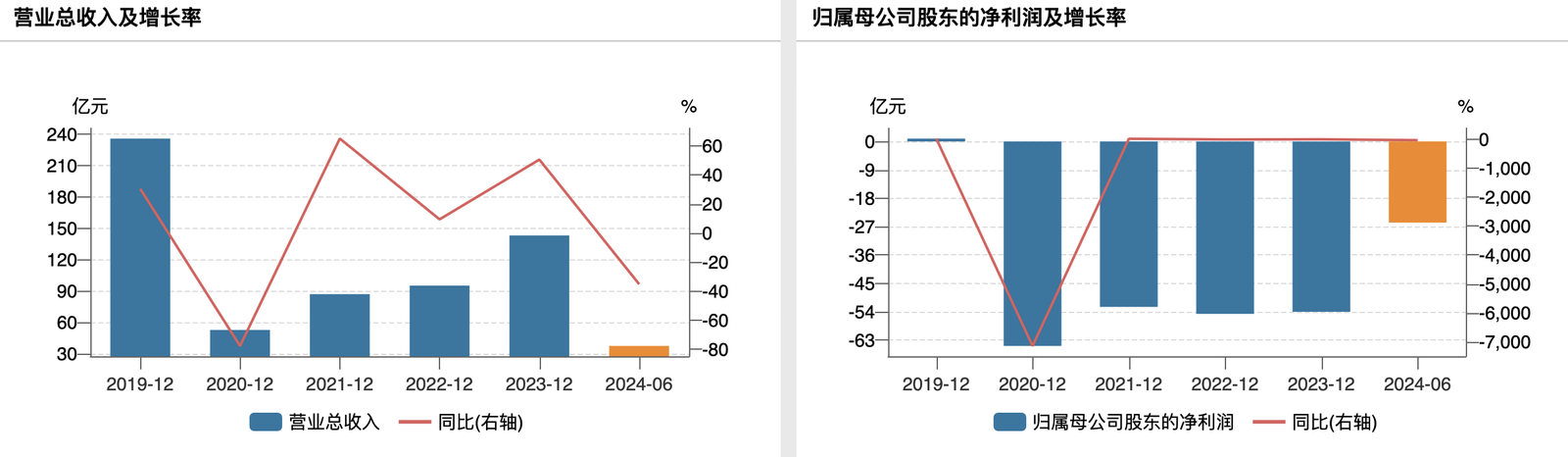

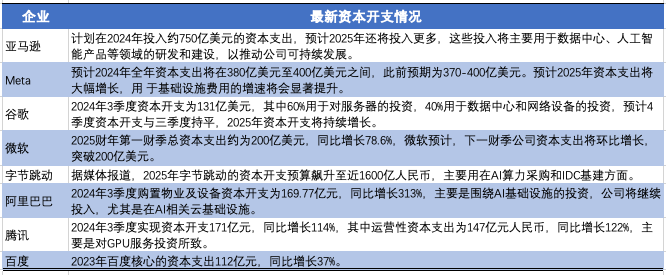

The latest institutional research shows that in the decline cycle of the past few years, the capital expenditures of the three BAT companies have experienced a significant downward phase. However, in the first three quarters of 2024, due to a new round of development momentum driven by AI, the development of the three cloud providers Expenditure has exceeded the level for the whole of 2023. It is expected that the full-year development expenditure may reach 15 billion to 20 billion US dollars, an increase of approximately 70% compared with 2023, achieving a historically high increase. It is expected that by 2025, the growth rate of domestic cloud providers will exceed that of overseas, and the growth rate of capital expenditure is expected to outperform overseas by 2025.

The latest capital expenditure situation of major domestic and foreign Internet manufacturers, compiled by the Kegubao column team

According to Huawei’s prediction, by 2030, the total global general computing capacity will reach (FP32) 3.3ZFLOPS, a tenfold increase from 2020, and AI computing (FP16) 864ZFLOPS, an increase of 4,000 times from 2020; the total number of global connections will reach 200 billion, and the global The total amount of data generated every year reaches 1YB, an increase of 23 times compared with 2020.

Guotai Junan data shows that in the first half of 2024, Huawei’s accelerator card share in the domestic smart computing market will increase to 17%, but Nvidia still holds 80% of the market share. Tianfeng Securities pointed out that with the antitrust investigation of Nvidia and the further export control of AI chips in the United States, the share of domestic computing power is expected to increase rapidly.

The computing power layout of China’s eight major computing power hubs in major cities, compiled by the Kegubao column team

The full text is read as follows:

For more exciting content, follow Titanium Media’s WeChat ID (ID: taimeiti), or download Titanium Media App

![[Dismantling of technology stocks]The latest research shows that domestic cloud manufacturers’ capital expenditures have achieved a historically high growth rate, and the growth rate in 2025 is expected to outperform overseas](https://takonews.com/wp-content/uploads/2024/12/spotify-1-150x150.jpg)

![[Dismantling of technology stocks]The latest research shows that domestic cloud manufacturers’ capital expenditures have achieved a historically high growth rate, and the growth rate in 2025 is expected to outperform overseas](https://takonews.com/wp-content/uploads/2024/12/Cover-image.webp-150x150.jpeg)