In August, the semi-annual reports of A-share photovoltaic listed companies were released. The leading companies suffered heavy losses and collectively declined in performance, all of which showed the difficulty of survival in the industry. The word “price” appeared most frequently in the annual reports of various companies. The “price reduction trend” that has lasted for more than a year has put great pressure on corporate performance. If prices continue to fall, the “big reshuffle” that was popular in the industry before and the prediction that “half of the companies will go bankrupt” are likely to become a reality.

If we look at the price trend of the photovoltaic industry chain throughout August, although the prices of products in most links are still pinned at the bottom or even continue to fall, the good news is that the prices of some silicon material products have begun to rise, and in the silicon wafer segment, after several months of production cuts, leading companies have simultaneously raised prices, allowing some practitioners to see the possibility of launching a “price counterattack war.”

Silicon materials: Prices of some categories have increased, but now show signs of stabilization and recovery

The silicon material segment experienced a roller coaster ride in the first half of this year. Prices rose first in the first quarter, but fell sharply in the second quarter. In contrast, the trend in the first month of the third quarter was relatively flat, with almost no increase or decrease.In August, prices of some types of products finally rose again..

From the data, according to the statistics of the Silicon Industry Branch of the China Nonferrous Metals Association, as of the end of August,The transaction price range of N-type rod silicon is 39,000-44,000 yuan/ton, with both the lowest and highest prices increasing. The average transaction price is 41,000 yuan/ton, up 2.5% from the end of July and 2.5% from the third quarter to date, but down 39.5% from the beginning of the year.;For N-type granular silicon, the transaction price was concentrated between 36,000 and 37,000 yuan/ton, with an average price of 36,700 yuan/ton, a slight increase of 0.55% from the end of July and a decrease of 37.8% so far this year;In addition, the transaction price range of recycled materials was 35,000-38,000 yuan/ton, and the average transaction price was 36,100 yuan/ton, which was the same as in July. There was no change in the third quarter as a whole, and it fell 40.1% from the beginning of the year; the transaction price range of P-type dense materials was between 33,000-36,000 yuan/ton, and the average transaction price was 34,300 yuan/ton, which was neither up nor down compared with July, and it has fallen 41% so far this year; the current transaction price range of P-type cauliflower materials is between 30,000-33,000 yuan/ton, and the average transaction price is 31,200 yuan/ton, which was the same as in July, and it has fallen 42.9% so far this year.

According to the observation of the Silicon Industry Branch,In the middle of this month, the silicon material segment saw a significant increase in volume, and the prices of new orders from some companies generally rose, laying the foundation for the price increase for the whole month.However, the progress of signing orders varies from company to company, and there are also differences in prices among major manufacturers. Many companies in the industry are still waiting and watching. In late August, prices were once again in a stalemate, and it is still unknown whether prices can continue to rise. InfoLink also analyzed that the rebound in silicon material prices this month may be due to the combined effects of companies’ continued cash losses, supply-side maintenance in the third quarter, and increased production cuts. However, whether the market can bottom out and rebound as expected still requires some time to wait and verify.

In addition, it is worth noting that Sichuan, one of the main silicon material production areas, has recently experienced high temperature power rationing, which has also affected the production capacity of silicon wafers this month. However, looking at the situation for the whole month, the increase in supply is still greater than the decrease, and there has been no obvious reversal of supply and demand.

Silicon wafers: The industry continues to reduce production, and leading companies begin to raise prices

The silicon wafer segment has always been greatly affected by overcapacity and low prices. After the segment began to cut production significantly in the second quarter, some results seem to have been seen this month. Although from a price perspective, the average transaction price of most categories is still lower year-on-year, the leading companies’ price increases still give the industry hope for a price counterattack.

According to statistics from the Silicon Industry Branch, the current transaction price range of P-type M10 monocrystalline silicon wafers is 1.1-1.25 yuan/piece, and the lowest price has dropped from last month. The average transaction price is currently 1.15 yuan/piece, down 6.5% from the end of July, and the decline in the third quarter is also 6.5%, which is 39.5% lower than the level at the beginning of the year; the current transaction price range of P-type G12 monocrystalline silicon wafers is 1.65-1.7 yuan/piece, and the average transaction price is 1.7 yuan/piece, which is the same as the end of July, down 1.2% from the third quarter so far, and down 43.3% so far this year;The transaction price range of N-type G10L monocrystalline silicon wafers was RMB 1.1-1.15/piece, and the average transaction price was RMB 1.11/piece, a slight decrease of 0.89% from the end of July. However, it is worth mentioning that the price of this product rose slightly last month. After the price reduction this month, the price is still higher than the June level, but it has also fallen by 39.5% so far this year.The transaction price of N-type G12 monocrystalline silicon wafers was anchored at 1.5 yuan per piece, down 6.3% from the end of July and down 9.1% from the third quarter to date.

As mentioned above, silicon wafers started to reduce production early. From the supply and demand pattern in August, the monthly output of silicon wafers was less than that of battery cells.TCL CentralLeading companies such as , Gogreen Solar and others continued to cut production, the supply and demand situation improved significantly, and corporate cash losses also decreased.

More importantly,On August 27, the two largest silicon wafer companies –LONGi Green Energyand TCL Zhonghuan announced price increases for silicon wafers, followed by Gogreen Solar,Shuangliang Energy SavingWhen the leading enterprises followed suit and raised prices, second- and third-tier enterprises also raised their quotations one after another.At the end of the month, the average price of N-type silicon wafers also showed an upward trend. From production cuts to price increases, the industry is currently looking forward to the silicon wafer segment being the first to get out of the downturn and usher in a continued price rebound.

Battery cells: Prices have not stabilized yet, and both N-type and P-type are falling

With the development of photovoltaic technology and the evolution of the industrial structure, battery cells have become an increasingly low-profit segment. However, in recent months, the already extremely low prices in this field have been unable to stabilize.

According to InfoLink’s statistics, as of the end of August,The transaction price of monocrystalline PERC (182 mm) was between 0.28-0.3 yuan/W, and the average transaction price was 0.285 yuan/W, which was 1.7% lower than the end of July, 5% lower in the third quarter, and 20.8% lower so far this year.The transaction price of another category of P-type monocrystalline PERC (210 mm) is between 0.28-0.29 yuan/W, and the average transaction price is also 0.285 yuan/W, which is also a decrease of 1.7% from the end of July and a decrease of 23.0% so far this year.As for N-type batteries, as the production capacity of mainstream TOPCon products continues to be released, competition has become increasingly fierce. Not only has the price reduction been greater than that of P-type, but the average transaction price has also been lower than that of P-type. As of the end of August, the transaction price of this product ranged from 0.27 to 0.29 yuan/W, and the average transaction price was 0.28 yuan/W, down 3.5% from the end of July, down 6.7% in the third quarter, and down 40.4% this year..

In fact, the price of battery cells, which has been at an extremely low level since July, once gave people a feeling that “there is no more room for decline”, but it continued to decline in the second half of this month. InfoLink believes thatThe recent price cuts are mainly due to the continued decline in component prices, and the lack of sufficient bargaining power in the battery cell segment, so they have no choice but to accept lower transaction prices.In addition, it is worth noting that as the upstream of battery cells, silicon wafer manufacturers have taken the lead in raising their quotations. If battery cells do not increase in price, the losses will continue to expand. However, at present, with the demand for terminal components unable to be released and prices continuing to fall, the road to a recovery in battery cell prices may be very difficult, and the performance of enterprises is likely to be further pressured.

Components: All categories continued to fall by more than 5%, and manufacturers found it increasingly difficult to survive

As the terminal most closely related to power stations, the price of component products has always attracted the most attention. This year, the wave of component price cuts has continued to surge. In the third quarter, not only did the price drop below 0.8 yuan/W across the board, but the unstoppable price reduction trend has also made manufacturers suffer.

According to data released by InfoLink, as of the end of August,The transaction price range of monocrystalline PERC modules (182mm, double-sided double-glass) is 0.67-0.8 yuan/W, and the average transaction price has dropped to 0.74 yuan/W, down 5.1% from the end of July, down 7.5% in the third quarter, and the decline has widened to 22.1% so far this year;The transaction price range of monocrystalline PERC (210mm, double-sided double-glass) dropped to between 0.72-0.8 yuan/W, and the average transaction price was 0.75/W, down 6.3% from the end of July, down 8.5% in the third quarter, and down 23.5% so far this year;For N-type components, the current transaction price range of TOPCon is 0.71-0.82 yuan/W, and the average transaction price has dropped to below 0.8 yuan/W this month, at 0.77 yuan/W, a sharp drop of 7.2% from the end of July, a 9.4% drop in the third quarter, and a 23% drop so far this year; the current transaction price of HJT is between 0.83-0.95 yuan/W, and the highest price has dropped to below 1 yuan/W this month, and the average transaction price has dropped to 0.9 yuan/W, a 5.3% drop from the end of July, a 14.3% drop in the third quarter, and a further decline of 26.8% so far this year..

In addition, according to the news released by Digital New Energy DataBM.com, some second- and third-tier component manufacturers are seeking to recover funds by selling components at low prices in order to repay debts or fulfill upstream equipment contracts, which further pressures component prices.Aixu Shares,RisenLeading manufacturers have once again lowered their component quotations, especially BC products that are competing for the market. The price drops are significant, which also has a certain impact on the overall market.

Excessive inventory has led to a “low price wave”, and the weak and stable demand and the release of N-type production capacity have continued to aggravate the contradiction between supply and demand. After accumulating inventory, component factories have stepped up efforts to sell off inventory, causing prices to continue to fall. The component link seems to have fallen into a “vicious cycle”. InfoLink also commented thatRecently, special price components below 0.7 yuan/W continue to disrupt market prices, and manufacturers’ price competition strategies are becoming more and more aggressive.Moreover, as for the future market trend, at least from the current production and installation situation, the situation of weak demand and oversupply may continue to intensify. Problems such as low-price orders, inefficient products, and inventory price drops are difficult to solve in the short term, and component prices are still far from bottoming out and recovering.

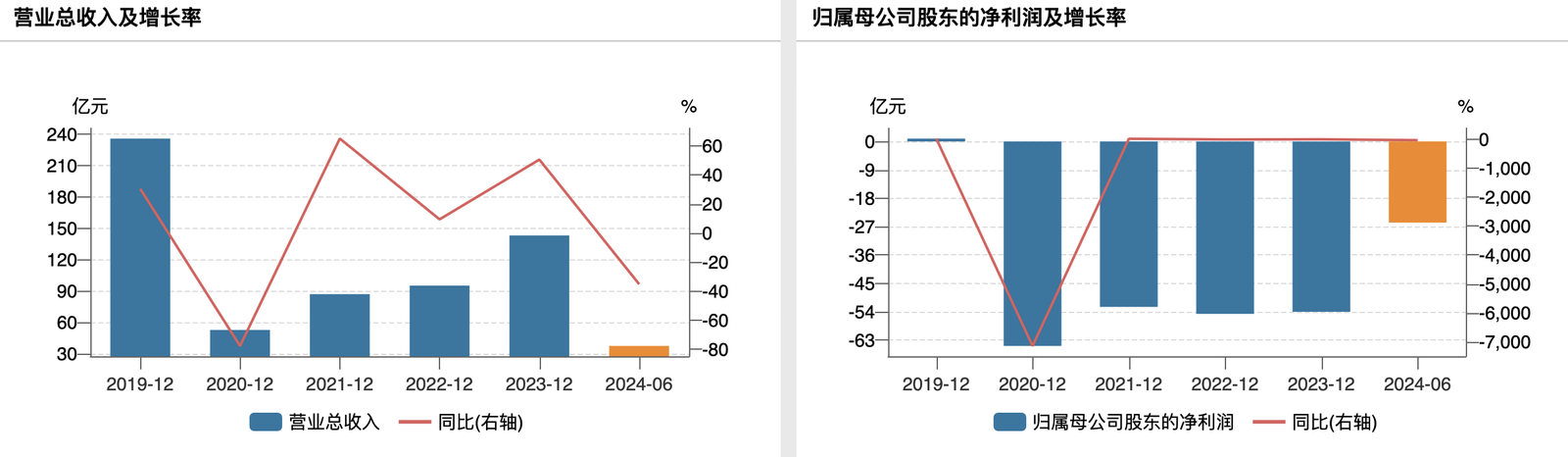

In the first half of this year, the photovoltaic industry has clearly entered another trough period. The top ten A-share listed companies (in terms of total revenue) saw an average year-on-year decrease in operating income of 16.4% and an average year-on-year decrease in net profit attributable to their parent companies of 69.9%.Tongwei SharesLongi Green Energy, and TCL Zhonghuan, the three leading companies, have all suffered losses of more than 3 billion. The industry situation is already very grim. If prices continue to be weak, the companies will only have a harder time.(This article was first publishedAtTitanium Media APP, author|Hu JiamengEditor |Liu Yangxue)

For more macro research information, please follow the Titanium Media International Think Tank official account:

For more exciting content, follow Titanium Media WeChat ID: taimeiti, or download the Titanium Media App